10 easy steps to investing without a financial advisor

Investing is one of the best things you can do for yourself and your family. Whether you’re a seasoned investor or just getting started this post is going to walk you through easy steps to investing without a financial advisor.

Don’t worry if you feel confused, overwhelmed, or just looking for more tips. It’s hard to question social norms that tell you to work harder, save more, and leave investing to the professionals.

We all just want to do what’s easiest in life.

But doing what you’ve always done, is guaranteed to produce the same results where you just can’t seem to get ahead in life.

As pointed out in an article by Dividend Power, the inequality of income distributions in the United States is rising.

You have to do something different. And this is your opportunity.

I know that you can start these easy steps to investing by yourself. And these easy to start steps steps to investing are sure to change your mindset and your life.

Let’s get started (remember the order matters).

Table of Contents

Step 1: Establish SMART financial goals.

SMART financial goals are specific, measurable, attainable, relevant, and time-bound.

These goals help you set up boundaries for your goals.

Now, take a moment to think about where you want to be in 10, 20, or even 50 years.

Where do you want to live? Do you want to be working? Do you want to travel? How much money do you need?

Let’s say you think it is going to take $75,000 to live every year in retirement. You then take that number and multiple it by the number of years you plan to live in retirement. Most of us want to retire by 60 and live at least another 25 years…at least I do.

That means I would need $75,000 X25 = 1,875,000 to live through retirement using the rule of 4%.

Now the rule of 4% just basically says you will spend 4% of your total nest egg each year and spend it all by the time you die.

But the way we invest, it’s unlikely you would pull $1.8 million out of the market and just live off it. We will continue to make money off our money (albite it would be less because we won’t keep everything in the market like we are now).

I would keep at least half of the money fully invested and the remaining in bonds. The invested money would be in safe stocks and should return anywhere from 8-10% annually.

That alone is probably going to be enough to live off.

Now you may be thinking I don’t need that much money. But you have to consider taxes and inflation.

It’s best to have too much than not enough. Go ahead and dream big with big numbers. Set this goal and make a plan to achieve it.

You can do achieve any goal with a plan.

The second half of Step one is to come up with the plan to reach your goal.

Again you should be using SMART.

Here you are going to be specific about how much to invest, for how long, and what types of returns you want to achieve.

Knowing the types of returns you want to achieve is going to help you determine which companies you want to invest in.

You will need to do research on all of the companies and ETFs that you are interested in owning. You will look at their performance over the last 1 month, 1 year, and 5 years.

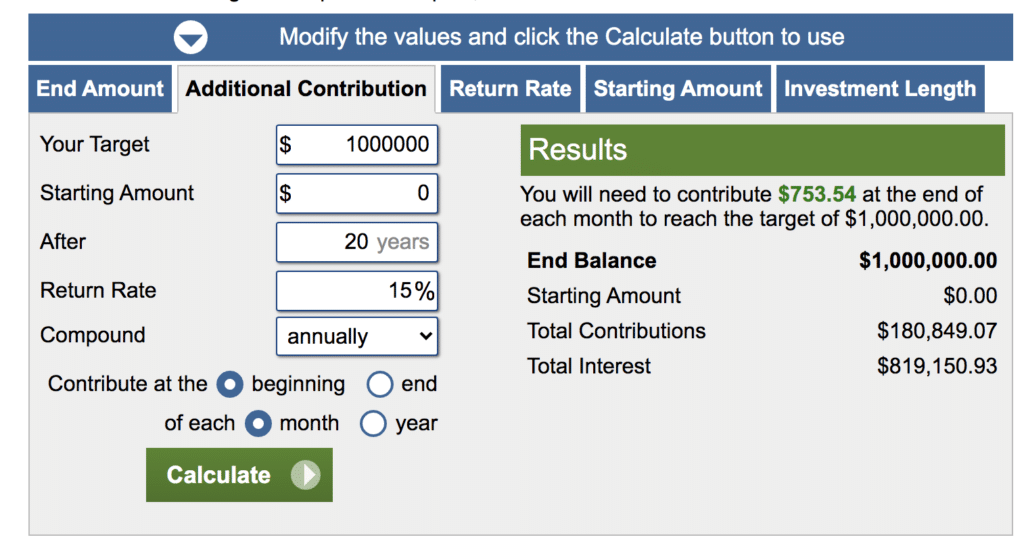

Check out this retirement calculator here from calculator.net.

Under the additional contribution table, you plug in how much you want to have (in dollars) and how long you have to reach that figure (in years).

Voilá you just calculated how much you need to invest every year to get there. See below for my example.

In my example. I want to have $1,000,000 in 20 years. I would need to invest nearly $754 a month for the next 20 years with a 15% return on investment.

Now remember, this doesn’t include dividends that I am earning.

So go ahead and think big in terms of your goals and work from there.

Check out the goal worksheet in my free budget tracker to help you get started. Be sure to add it to your planner or file system.

Always remember to use SMART goals and have a SMART plan to reach those goals.

Step 2: Create a personal budget

I’m sure you saw this one coming. Everyone needs a personal budget. A budget ensures that your money goes to all of the right places.

No one likes to come to the end of the month without enough money to save/pay themselves, pay bills, or have fun.

Here are the benefits to personal budgeting:

- Prevents overspending

- Gives you power over money

- Allows you to make plans for big purchases without anxiety

- Reduces stress of not having enough money

- Allows you to establish goals

- Helps you identify money problems before they occur

- Increases motivation to save, pay off debt, and give more

Types of Budgets:

- Zero-sum budget (Every dollar budget)

- 50/20/30 budget (50% goes to fixed expenses, 30% to variable expenses, 20% to financial goals)

- The anti-budget budget (calculate your expenses and savings, everything that is left after those items are paid is your free spending money)

- The envelope system budget (used to prevent overspending for personal items, groceries, gas, eating out for things you can pay in cash).

- The no budget-budget (doesn’t exist. You either have a budget or you don’t. And yes, every one needs a budget.)

Now let’s move into the next steps to investing!

Step 3: Discover work investment plans (401K, Self-employed 401K, and Health Savings Account)

Get with your Human Resources department and ask about investment plans offered by your company.

You want to be proactive and seek this information because you may only be able to enroll at certain times of the year.

The following are a list of questions that you need to ask:

- Are the contributions taxed now (Roth) or later (Traditional)?

- Does the company match contributions?

- When are company matches vested?

- What are the max contributions?

- How can you monitor the account?

Max these work investment plans first!

Because these are typically free money from your employee. If you’re going to work for someone else, you might ask well maximize your earnings.

Step 4: Open an investment account

Now this step isn’t hard, but it does require a little research.

What features are you looking for in an account?

Do you want something with an easy to use app?

Do you want something with robo-advisors?

Do you want something with a lot of training and educational material?

You have many options.

I personally love TD Ameritrade, Charles Schwab, and Acorns. And I use each account for a different reason.

TD Ameritrade is my primary taxable trading account. Even though I am a long-term investor, I still need an account to put money in after I have maxed my Roth IRA.

TD Ameritrade has great educational resources and the interface is easy to use. I’m telling you anyone can do it.

Pros: No cost to make trades. No minimum account balances or transfer amounts.

Cons: There may be fees when a company’s stock splits or falls off the NYSE. Have to have a minimum $3K in the account to receive live training from a broker.

Next, Charles Schwab. This is where I house my Roth IRA. I like Charles Schwab for the fractional shares and ease of use. I think Charles Schwab offers a little more upfront information about the market than TD Ameritrade but it doesn’t seem to promote individual stock trading as much.

Pros: No cost to make trades. No minimum account balances or transfer amounts.

Cons: The watchlist is a little less intuitive and helpful than TD Ameritrade’s watch list.

Lastly, I like Acorns. This is an automatic robo-investing account. I use it like a savings account but I don’t take money out of it.

With Acorns you are not able to pick which stocks your money is invested in. But they tend to follow the market (S&P 500) pretty closely.

Pros: Automatic, easy

Cons: No options for investments

Pay yourself first

Now I want you to go back to budget and make sure that you are paying yourself first.

How much money do you have for savings?

You want to aim for 10% but there may be months when this is not possible.

At the beginning of the month or at the beginning of the pay period, you want to transfer the money automatically from your checking account to your investment/savings accounts.

I recommend having a high yield savings account with sinking funds (or separate accounts) for:

- Emergencies

- Big purchases

- Gifts/holidays

- Vacations

Step 5: Pay yourself first

This is not optional. You must pay yourself first. If you are not making enough to pay your bills after you pay yourself, you need to reduce expenses and increase income.

Start by taking a look at all of your:

- Subscriptions

- Eating out

- Extras-cable, car, clothes

Decide what you can cut out and get rid of it. It doesn’t have to be forever, but for now, it has to go.

Make a plan to make more money. What can you sell on Etsy? Can you get a second job delivering food? Would you make a good tutor?

There are so many ways to make a little extra money.

Now is the time to humble yourself and get to work.

You cannot reach financial freedom without paying yourself first.

You have to be investing. And investing takes time.

Investing is a long-term game where you need time to help compound your money.

Paying yourself first is easy. You can either set up a reminder on your phone’s calendar or you can set up an automatic money transfer from your brokerage account.

Just remember when the money is initially transferred, it is put into a cash account. It doesn’t automatically get invested. Of course, you can keep it as cash if you do not have enough to invest in the company that you want to.

But in general, transferring money alone isn’t enough. You need to invest that money. You can consider accounts with fractional shares like those at Charles Schwab or you can invest in exchange traded funds (ETFs) that represent a collection of the best companies in a specific sector.

Be sure to have a budget and a personal investment strategy to be the most successful at building financial freedom and generational wealth.

Step 6: Learn, learn, learn

You cannot be successful without taking time to learn every day. You have to do it.

Reading 10 minutes a day is one of the best things you can do for yourself.

Set a reminder on your calendar and just do it.

Here is a list of my favorite books:

- The Automatic Millionaire – David Bach

- Rich Dad Poo Dad – Robert T. Kiyosaki

- The Little Book of Common Sense Investing – John C. Bogle

- The Intelligent Investor – Benjamin Graham

- The Dhando Investor – Mohnish Pabrai

- Invested – Danielle Town

- Money, master the game – Tony Robbins

- The Total Money Makeover – Dave Ramsey

I have read each of these books and highly recommend them.

Reading is guaranteed to simulate your mind and your attitude.

Go ahead and set that daily calendar reminder now.

Step 7: Take a course

Equally as important but similar to learning, I recommend everyone take a course on investing.

More specifically, fundamental analyses.

This will teach you about the things you look for when buying stocks.

Warren Buffet’s Top 2 rules:

- Don’t lose money

- Don’t’ forget rule 1.

When buying stocks, you want to focus on companies that you understand 100%.

For example, I do not understand cryptocurrency. Therefore I cannot invest. Perhaps, if I took the time to learn, I would be able to invest it. But as it stands today, it is not for me.

When looking at the company, do you see a competitive advantage, do you like the management, is the company innovative?

You want to focus on companies that you know are going to be around and be successful in 20 years.

Start by looking at companies that you are already buying from.

Who makes your phone, computer, clothes, food?

Research companies that meet your needs (food, clothes, commodities), wants, and interests (hobbies).

The first step in research is looking at their cash flow and balance sheets. How much debt does the company have? Is the revenue growing?

You will learn all kinds of ratios to help you with investing through a simple investing course.

Take a look at a free 5 day course by Phil town at Rule One

He focuses on the 4 M’s (Meaning, Moat, Management, and Margin of Safety).

This course is free and very thorough. It will not disappoint.

I also recommend TD Ameritrade’s fundamental analysis course (free if you have a free account).

Step 8: Buy quality investments

You are primed with knowledge.

Start by building your watchlist.

Make sure that you really want to invest in a company for the long-term.

If you don’t feel good about the company or you are questioning your decision, go back to the fundamental analysis or just consider buying “the market” aka a simple EFT fund that tracks the Nasdaq or the S&P 500.

These funds will never go to zero and the only time you could lose money would be if you took your money out too early. These funds are constantly rebalanced to have the top businesses and get an accurate reflection of the state of the market.

Lazy retirement portfolios are another option. The Bogleheads 3 fund portfolio tracks both U.S. and international stock market and U.S. Bonds without you having to pick stocks. Everything is done for you and low-risk.

Just remember you can keep cash in your investment account. You can build up for a company with expensive shares like Apple (AAPL) which is over $3K for just one share at the time of this post.

Do not buy stocks because your friends are buying stocks.

Buy companies that you believe in and want to own. If you’re not ready to pick stocks think about index funds that track the broader market. Just make sure they have low fees.

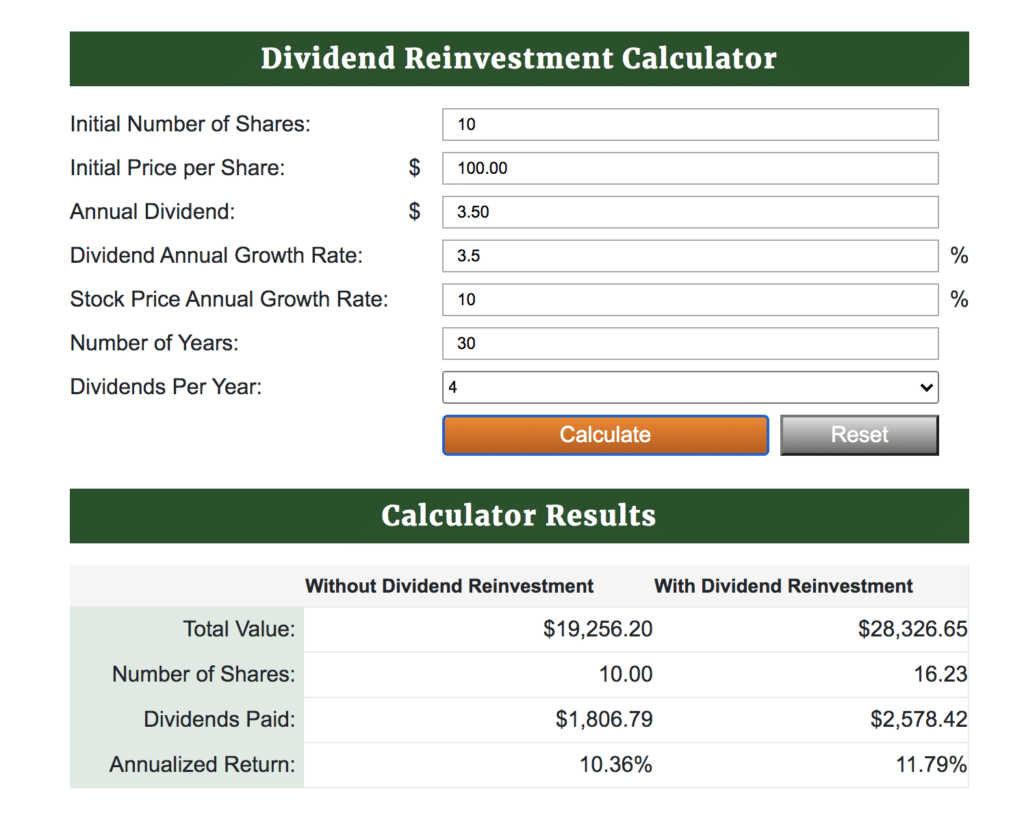

Step 9: Make sure you are reinvesting dividends

This one is easy. You need to be reinvesting dividends.

You have to check the box or hit a button within your account that says to reinvest dividends.

It does not happen automatically.

Please go in right now to make sure that dividends are being reinvested.

Initially your dividends may just be a few dollars, but years from now they could be thousands of dollars.

Not reinvesting thousands of dollars with cost you thousands of dollars compounded.

Take a look at the graph below to see the cost of not reinvesting dividends on a stock that costs $100 and you own 10 shares (that is a $1,000 initial investment).

So you $1,000 investment cost you nearly $10k in additional gains if you failed to reinvest dividends.

Imagine if you had 5 investments like this one. That’s $50K.

Just think about it.

Step 10: Keep going, don’t stop

Compound interest matters. Invest early and invest often.

You may not notice the initial gains in your account but give it a few years and you will be blown away. Millionaires are made everyday in the stock market.

Be sure to talk to those people in your world. Knowledge is power, spread it throughout your community. There’s nothing wrong with talking money to your friends and family. It’s all about your mindset.

Do you really want to help your friends and family or not?

Recap

So there you have it…10 easy steps to investing without a financial advisor.

You cannot successfully invest in things you do not fully understand. And you cannot successfully invest without a budget or SMART financial strategy. Investing requires you to be in a position to save money, invest often, and reevaluate your portfolio for the long-term several times a year.

Nobody got rich saving. Stay in the game by reading, listening to podcasts, and talking with people around you. I know you can do it if you follow these 10 steps to investing in order.

Please comment below, have you tried these steps to investing.

Theresa is a personal finance blogger. She writes content for busy professional women to take control of their money and investments. She enjoys reading, traveling, cooking, and writing. Her work has been featured on GoBanking Rates, Your Money Geek, Savoteur, the Corporate Quitter, Thirty Eight Investing, and more.